Email Us

A Most Curious Market Rally

Why Stocks Have Rebounded in the Face of Historic Unemployment?

“I’m glad the S&P 500 has shot up from where we were in March, but I’m concerned over how high the unemployment rate is. How can the market be doing so well with so many out of work?”

This is a common question, and the apparent disconnect between the stock market and the broader economy has been a controversial topic – especially over the last few months.

Reason No. 1: The Stimulus

Between the $2 trillion CARES Act, various smaller bills and the Federal Reserve’s sizeable response (see below), we have seen a larger and faster injection of stimulus than nearly any other time in history. While there is a lot going on beneath the surface, this infusion of cash has supported markets in two ways:

The $1,200 stimulus checks and super-charged unemployment benefits put money in the wallets of the people who needed it the most. To understand why that’s important, let’s look at how recessions undercut the economy. Recessions often feature a death spiral that looks something like this:

In the current recession, the government tried to stop this spiral by replacing Americans’ lost income with stimulus money. And it seems to be working: Recent studies have shown that not only has COVID-19 not caused a dramatic spike in poverty, but the average American actually may have had more money available over the past few months than pre-COVID. This kept bills paid, people spending (to an extent) a

nd consumer confidence from tanking – all key to a rising stock market. The expectation of more stimulus this summer has buoyed stocks even further.

Through lower interest rates, quantitative easing and other programs, the Federal Reserve has created a favorable environment for equities. Low interest rates drive money into the stock market by making bonds less attractive, while an increase in liquidity (i.e., money) via Federal Reserve policies often finds its way into financial assets (i.e., stocks)

Reason No. 2: The Markets Are Forward-Looking. Among many other things, the Fed also provided support to fixed income markets and kept a health crisis from becoming a credit crisis, which would have been a major negative for equity markets.

The stock market by nature is a forward-looking system, while economic data like unemployment are always looking backward. This can create a mismatch at times. For example, while April 2020 unemployment rates were at Great Depression levels, the stock market was shooting higher – largely based on the increasing likelihood of a vaccine by 2021. (Stocks’ forward-looking nature is also why markets usually begin their rebound well before a recession is over.)

Relatedly, the initial 2020 market crash was as much about uncertainty as anything. In mid-March, respected health officials were predicting worst-case scenarios of overrun hospitals and millions of people dying, all with no evidence that we may ever get a vaccine. Today, we have a much stronger grasp on the virus itself, effective treatments and protective behaviors – and we have several vaccine candidates deep in trial. While the spread of the virus remains troubling, the worst-case outcomes are likely off the table. Thus, some of the recent rally was simply walking back a crash that was at least partially predicated on now unlikely worst-case scenarios.

Reason No. 3: Economic Data Is Bottoming

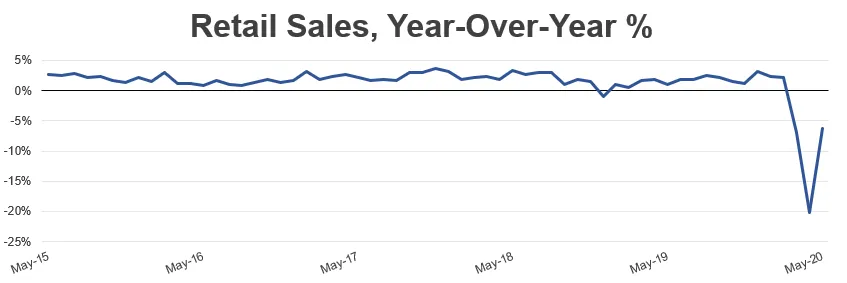

While the initial rally off of the lows was led by defensive sectors (such as healthcare and utilities), out-performance quickly shifted to beaten-down, cyclical sectors like airlines, cruise ships and energy. Though they have faltered in recent weeks, their recovery coincided with an increasing number of signs that economic data was bottoming as re-openings progressed. Strong May jobs figures, resilience in housing, minor upticks in air travel and restaurant data, global PMIs, shipping, retail sales – the economy is now showing signs that a durable bottom in the data has formed, giving hope that a relatively broad recovery is possible.

Further, while second wave fears are certainly justified, we think it’s unlikely that future lock-downs will reach the breadth and penetration we saw with the first wave. Though the speed and length of the recovery are worth debating, we are confident we’re now at least heading in the right direction.

Reason No. 4: The Market Was Made for This Crisis

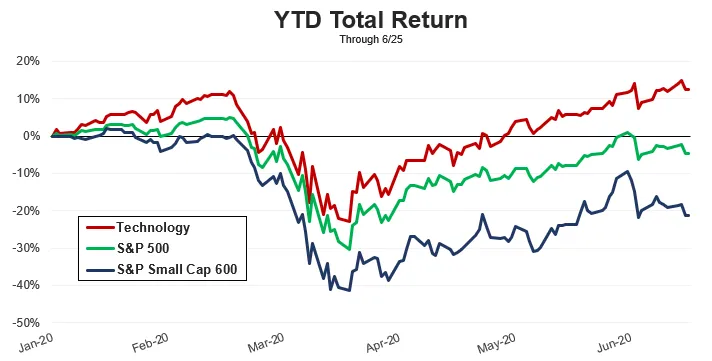

The S&P 500 is made up almost entirely of large- and mega-cap firms, and its biggest sector by far is technology. We’d argue that this crisis in particular was suited to larger firms that could better withstand the lock-down and are primed to gain market share in the post-COVID world. Reflecting this reality, the S&P 500 is essentially flat for the year, compared to a ~20% drop in the S&P Small Cap 600.

The technology sector is also uniquely suited to this crisis, with products and services tailor-made for a pandemic lock-down, like online shopping, social media, work-from-home necessities, music/video streaming and gaming. The coronavirus accelerated many trends already in place, resulting in relative out-performance and heavier weightings in technology companies. This was not the case for the largest sectors in other recent crashes (such as the 2001 dotcom bubble or the 2008 housing crisis), when the biggest sectors were the most vulnerable and hindered the market much further.

Reason No. 5: The S&P 500 Is Global

The S&P 500 gets roughly 40% of its revenue from overseas, and many U.S. supply chains are inextricably linked to foreign countries. While this pandemic was a global event, other countries (particularly China and South Korea) emerged from lock-down earlier and with fewer cases and hospitalizations. As their economies ramped back up ahead of ours, the S&P 500 would likely benefit even if the average American worker would not.

This is certainly not to say stocks cannot go lower in the near term – they absolutely can. We face real risks, both virus-related and otherwise, that could shake markets if they develop unfavorably. But the historic volatility of the last few months has simply reinforced some of our key investing beliefs: the difficulty in market timing, the benefit of owning a diversified portfolio, having a sound financial plan in place to deal with sharp market moves. And that is the true benefit of expert financial advice.